One fund which has absolutely floored me with its amazingly consistent performance in all types of market, especially in the last 8 quarters or so is the EDELWEISS ABSOLUTE RETURN FUND.

I have ensured that every single client of mine has got an exposure to this fund.

And, in fact, whatever maybe the Risk Profile of an Investor, this Fund is a MUST HAVE.

Why am I so sold on this fund?

Whats so special about this strange sounding Absolute Return fund.

Lets analyse.............

WHAT'S IN A NAME?

I have ensured that every single client of mine has got an exposure to this fund.

And, in fact, whatever maybe the Risk Profile of an Investor, this Fund is a MUST HAVE.

Why am I so sold on this fund?

Whats so special about this strange sounding Absolute Return fund.

Lets analyse.............

WHAT'S IN A NAME?

Edelweiss Absolute Return Fund may "sound" like a liquid fund because of the

"absolute" in its name. But,

its a Equity Fund and surprisingly its benchmark is Crisil MIP Blended Index

Fund!.

Edelweiss Absolute Return Fund is an ideal fund for those investors who

want stable returns with low volatility.

OBJECTIVE :

It stated objective to capture 60% of Nifty upside and limit to just 20% of

Nifty downside

The Primary Objective of the Edelweiss Absolute Return Fund is to generate Absolute Return over a longer period of time without the accompanying volatility usually associated with Equity Funds.

Its aims to achieve this by avoiding risk and by taking hedging and

arbitrage positions, special situations, Nifty Short, and also FDs (yes, you

read it right...it is Fixed Deposits!)

Special Situations, according to Edelweiss people, mean IPOs, Delistings, Equity Buy Back,

Open Offers, Mergers, Acquisitions, etc.

Special Situations aims at providing good trades which yield absolute returns over short periods. Its Special Situations has generated returns ranging from 3% to 25% Absolute Returns. The Fund also does not shy away from taking exposure to Money Market Instruments and IPOs too.

Special Situations aims at providing good trades which yield absolute returns over short periods. Its Special Situations has generated returns ranging from 3% to 25% Absolute Returns. The Fund also does not shy away from taking exposure to Money Market Instruments and IPOs too.

Its hedging strategy is mostly dependent upon the basis of Corporate

actions rather than on Market Valuations and this has helped the Fund in protecting the fall in NAV during

market downsides.

Since the fund's strategies of Equity Investment for Long Term, Special

Situation Investments and, Hedging strategies and Derivative trading are not

co-related, the volatility of the Fund drastically comes down.

Scheme

Name (25-May-2015)

|

Returns*-

Edelweiss Absolute Return Fund

|

||||||||

1

Month

|

3

Month

|

6

Month

|

1

Year

|

2

Year

|

3

Year

|

5

Year

|

Since

Inception

|

||

Edelweiss

Absolute Return Fund(G)

|

1.83

|

2.00

|

6.72

|

24.45

|

19.64

|

16.92

|

12.54

|

11.67

|

|

Crisil

MIP Blended Index ( ARF Scheme Benchmark)

|

0.51

|

0.75

|

4.29

|

12.87

|

8.89

|

10.76

|

8.65

|

8.57

|

|

Crisil

Balanced Fund Index

|

1.32

|

-1.70

|

1.34

|

14.20

|

14.90

|

16.20

|

10.48

|

13.40

|

|

CNX

Nifty Index

|

0.78

|

-4.53

|

-1.10

|

13.54

|

18.25

|

19.37

|

11.73

|

14.63

|

|

PERFORMANCE :.

The fund has managed to beat its Benchmark quite consistently by a good margin and that too while taking less risks!

The Edelweiss Absolute Return Fund has NOT given any negative returns if

the investor has stayed for more than 2 years and upside is in line with Nifty!

The Fund has participated in its stated objective of capturing 60% market

upside and limiting to 20% of Nifty Downside splendidly.

Period-wise

performance

|

2010

|

2011

|

2012

|

2013

|

2014

|

Rolling

12M till 30th

April 2015

|

CAGR

(Frm '10)

|

Volatility

(Frm '10)

|

Edelweiss

ARF

|

13.3%

|

-2.3%

|

12.0%

|

9.4%

|

29.0%

|

33.9%

|

12.1%

|

7.0%

|

Crisil

MIP Blended Index (Benchmark)

|

7.0%

|

1.7%

|

12.1%

|

4.4%

|

16.8%

|

15.1%

|

8.2%

|

3.9%

|

Crisil

Balanced Fund Index

|

13.6%

|

-14.4%

|

21.3%

|

6.0%

|

25.3%

|

19.4%

|

8.9%

|

11.2%

|

Nifty

Index

|

18.0%

|

-24.6%

|

27.7%

|

6.8%

|

31.4%

|

22.2%

|

8.9%

|

16.9%

|

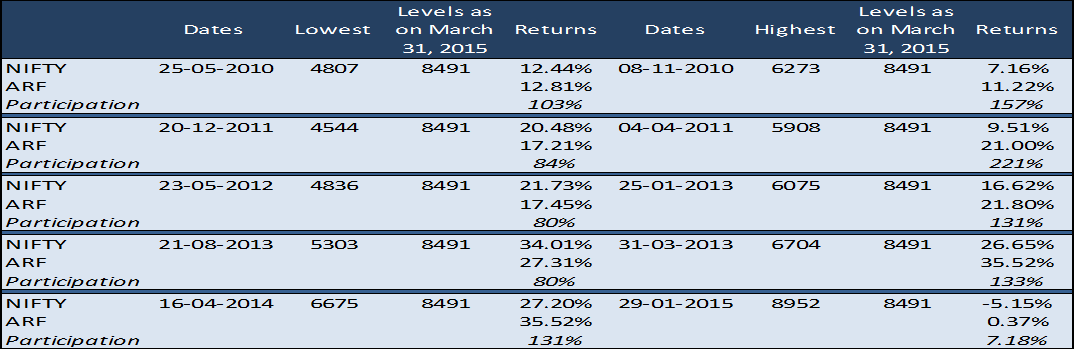

The Fact the Fund has been able to beat Nifty even during market upsides is

clearly captured in the data shown alongside....whenever an investor has

invested in Edelweiss Absolute Return Fund at the Lowest Level of Nifty, he has

made more money in this Fund than Nifty.

A Low Volatility fund

Its most unique and most attractive part is that when the Nifty/Sensex

falls, the Fund's fall is closed to MIPs inspite of being an Equity Fund.

DIVIDENDS :

Edelweiss Absolute Return Fund has been paying regular uninterrupted Quarterly dividend since the past 18 quarters. Its been paying about 2.2% which is eqvivalant to 8.8% Tax Free Dividend.

And it even paid 3% dividend in Jan 2015.

Edelweiss Absolute Return Fund has been paying regular uninterrupted Quarterly dividend since the past 18 quarters. Its been paying about 2.2% which is eqvivalant to 8.8% Tax Free Dividend.

And it even paid 3% dividend in Jan 2015.

FOR WHOM :

1. This Fund is for those who want equity risk without the accompanying volatility.

2. The Fund is especially suitable for Investors who have a lumpsum in hand and are unsure of where to invest and could look at this fund as short to medium term alternative.

1. This Fund is for those who want equity risk without the accompanying volatility.

2. The Fund is especially suitable for Investors who have a lumpsum in hand and are unsure of where to invest and could look at this fund as short to medium term alternative.

3. Good alternative to Fixed Deposits not only in terms of Returns but Taxation too.

4. New Investor to Equities who want to get a feel of Equity flavor.

5. An investor who is looking for consistent and stable return.

5. An investor who is looking for consistent and stable return.

WHAT SHOULD YOU DO :

Please treat this Fund as a MIP rather than a Equity or a Debt fund.

Please treat this Fund as a MIP rather than a Equity or a Debt fund.

If your time horizon is more than 18 months but less than 5 years, you

should look at this fund.

It is one of those rare funds which has given complete satisfaction to me

and my clients both in Bull and Bear Periods.

Especially their Prepaid SIP concept is something which every AMC should

look at replicating.

To understand how Prepaid SIP works, please click

When a Fund not only protects you during downside but also participates in

Upside, do you need to look at anything.

If a client comes to me and wants only one fund it will be EDELWEISS

ABSOLUTE RETURN FUND.

Also visit http:/http://goodinsuranceadvisor.blogspot.in/